Think back to your college or high school graduation. Do you remember dreaming of a big salary and a corner office because you thought a good income would make you rich? Once you were on your own, you probably discovered the marketplace only offered minimum wage and a middle-row cubicle right out of the gate.

How is your income now? Maybe you’re making a lot more or simply enjoying a satisfying career that pays an average salary. But do you ever think about the difference between income and net worth? And why does it matter?

In this article, I will explain the differences between income and net worth, and I’ll show you what those differences mean for your nest egg. I’ll even give you a tool to help you calculate your net worth to see if you’re on track to enjoy a dream retirement.

What’s the difference between income and net worth?

Let’s pretend Katie is a marketing executive who makes $150,000 a year and has a net worth of $20,000. Her friend Lacy is a schoolteacher who makes $45,000 a year and has a net worth of $250,000. Who has more wealth—the marketing executive or the schoolteacher? You got it. Lacy the schoolteacher actually has more wealth because she has a higher net worth than her friend Katie.

Be confident about your retirement. Find an investing pro in your area today.

That’s because when it comes to wealth, it really doesn’t matter how large your income is. Yes, you can build wealth faster with a larger income, but at the end of the day, your income doesn’t guarantee you’ll have a big nest egg when you retire. You have to save and invest that income throughout your career, no matter how much you make.

"Your income doesn’t guarantee you’ll have a big nest egg when you retire. You have to save and invest that income throughout your career, no matter how much you make." —Chris Hogan

So, what’s the difference between income and net worth? And how can those differences affect your retirement future? Let’s find out!

What is income?

The IRS defines earned income as all the taxable income and wages you get from working.(1) You earn income if you work for someone who pays you, or if you run a business or a farm. But income alone doesn’t make you wealthy. You could make $1 million a year and spend $2 million—meaning you’d be in debt up to your eyeballs. Or, you could earn $50,000 a year and retire a millionaire if you plan and save throughout your entire career.

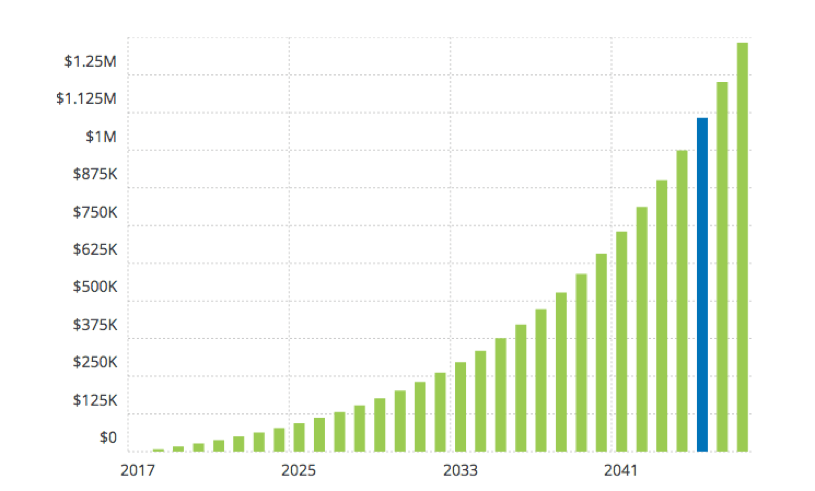

A quick calculation shows that a debt-free person who earns $50,000 annually and invests 15% of their income for 30 years could have almost $1.4 million saved for retirement. On the other hand, a person making twice that income who never invests even a small portion of it will likely come up short in retirement.

*The blue bar indicates this person’s million-dollar year.

A new financial buzzword describes this demographic of high-income earners who have little net worth. They’re called "Henrys," or "high-income earners not rich yet."

Equifax studied a group of "Henrys" who are under 55 years old, earn annual incomes of more than $100,000, and haven’t hit assets of $1 million. The study said student loans and car debt were barriers keeping "Henrys" from saving more for retirement.

Untamed discretionary spending—averaging $68,000 a year—also appears to keep "Henrys" from building wealth.(2)

People, a large income doesn’t necessarily lead to large net worth. And since we’re on the topic of income, let’s explore the difference between gross income and net income.

"People, a large income doesn’t necessarily lead to large net worth." —Chris Hogan

Gross income includes your pre-tax, pre-deduction wages. For example, if you earn $50,000 a year and get paid monthly, your gross pay is $4,166. Net income is what you actually bring home after taxes and payroll deductions, like Social Security and 401(k) contributions. Your monthly net income could look something like this: $4,166 (gross) - $1,200 (taxes/deductions) = $2,966 (net).

Practical takeaway: Your income is your biggest wealth-building tool—so use your paycheck to your advantage! Pay off debt as soon as you can and start investing 15% of your gross income for retirement.

What is net worth?

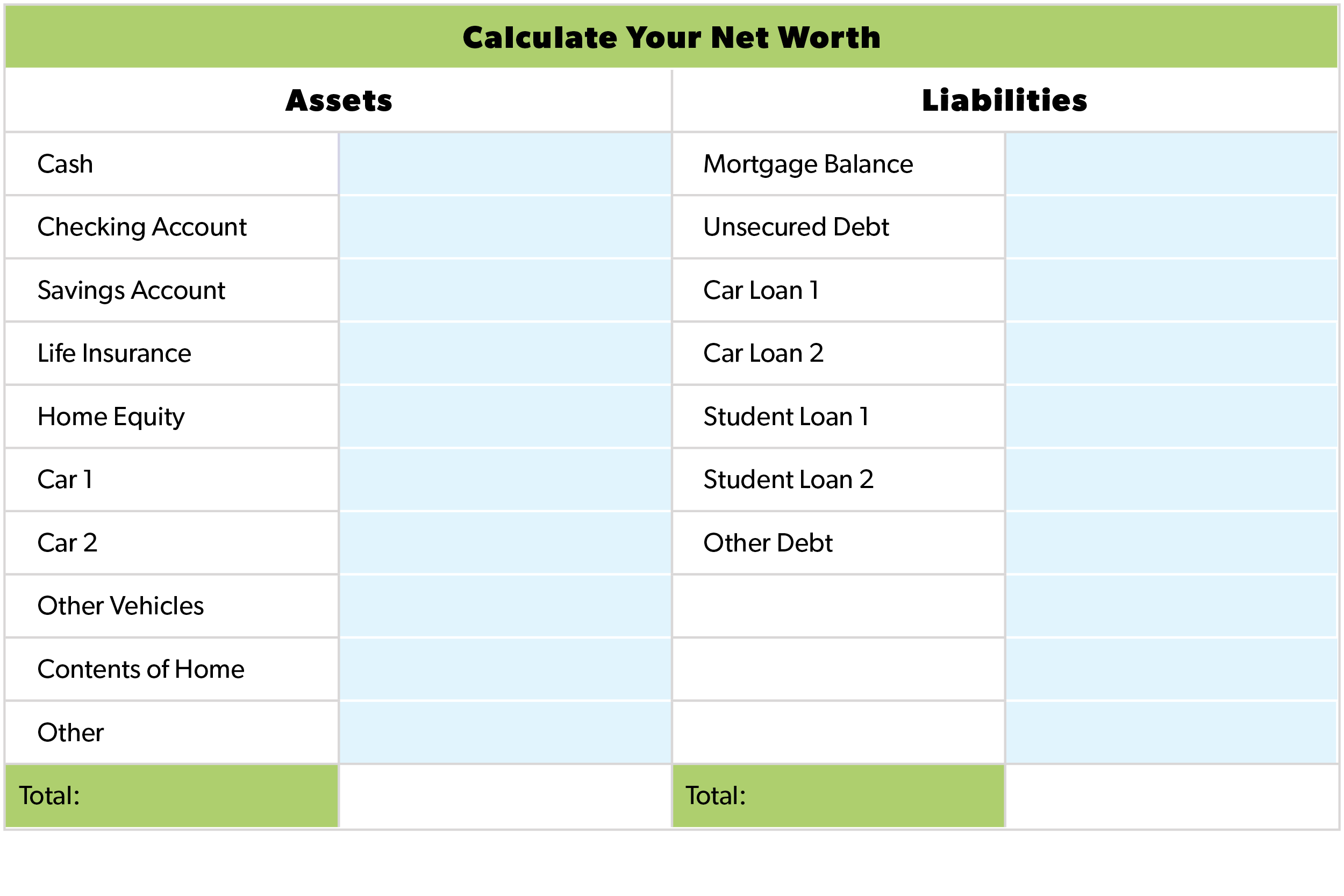

Net worth is what you own minus what you owe. In other words, the total value of your assets minus your debts equals your net worth. For example, if you own a home worth $300,000 and you owe $100,000 on it, you have $200,000 in equity toward your net worth. To calculate your total net worth, add up all the things you own and subtract all the things that you owe money on.

According to the U.S. Census Bureau, the median net worth of American households is $80,039. The majority of that wealth comes from home equity, followed by 401(k) and Thrift Savings Plan accounts, then IRA and Keogh accounts.(3) Business Insider reports the following breakdown of median net worth by age.(4)

- Under 35: $6,676

- 35–44: $35,000

- 45–54: $84,542

- 55–64: $143,964

- 65–69: $194,226

- 70–74: $181,078

- 75 and up: $155,714

So how do you stack up? You can use my Net Worth Calculator to calculate your net worth and gain insight into how many assets you really have. Remember, your income alone will not provide an accurate snapshot into your financial health. That’s why it’s good to know your net worth.

Now calculate: ASSETS TOTAL - LIABILITIES TOTAL = NET WORTH.

Once you calculate your net worth, you might be surprised to find out how much you have—or don’t have. In any case, there are ways to improve your finances and grow your wealth. Listen to Ron and Colleen from Los Angeles, California, share how they got serious about their money, paid off $123,000 of debt in 18 months, and ended up millionaires.

When do you become a millionaire?

You’re a millionaire when your net worth—not your income—reaches $1 million. You might have heard the phrase "cash millionaire." That means a person’s net worth exceeds $1 million, and $1 million of it is in liquid assets they can get a hold of quickly. That money isn’t tied up in a business or home or those kinds of things. That’s what you’re after in the long run.

You might think millionaire status is out of reach, but the characteristics of an average millionaire just might surprise you. When I talk to millionaires about their success with money, they don’t mention an inheritance or winning the lottery. They talk about smart saving, wise spending and investing practices, and a simple way of life.

Some other common habits include:

- They read a ton. Millionaires usually can’t tell you the latest drama on reality TV because they’re busy learning, growing and using their time wisely.

- They say no to instant gratification. Millionaires have no problem buying used cars, wearing $30 jeans, and buying owning modest homes. They care more about sensible spending than keeping up with the Joneses.

- They despise debt. Millionaires get out of debt and stay out of debt. Instead of owing money, they invest it.

- They budget and have a plan. Millionaires maintain a monthly written budget. They also get help from an investing professional so they can prepare well for retirement.

- They are generous. Millionaires understand that they are blessed to be a blessing. Millionaires give to their churches, charities and causes they care about.

See how ordinary people built extraordinary wealth in my new book, Everyday Millionaires.

Did you just get a net worth wake-up call?

You’ve learned that income is what you earn from working and that net worth is the value of your personal assets minus any debt. Now you should be able to crunch some numbers to determine where you stand financially. Are you making a great salary but have nothing to show for it? Or do you have an average salary and want to change your spending habits so you can invest and save more for retirement?

The good news is you’re the one in the driver’s seat. You can make the necessary changes to your finances so you can enjoy the retirement of your dreams. Start by talking to a financial advisor who can help you create a game plan for investing. If you need help finding a professional near you, check out the SmartVestor program.

Now get to work. Your future is at stake!

ABOUT THE AUTHOR

Chris Hogan

No comments:

Post a Comment